On February 24, Russia attacked Ukraine, bombarding multiple cities, and killing soldiers and civilians. Russia’s attack plunged Europe into one of its most serious security crises since World War II. As a result, President Joe Biden, European leaders, and other US allies announced severe sanctions, targeting major Russian financial institutions and elites, and blocking technology exports to Russia. The hope was that these measures would isolate, ostracize, and contain President Vladimir Putin’s Russia.

However, the success of such sanctions depends on whether those assets held outside Russia can be identified and are vulnerable to confiscation. Not all sanctions effectively resolve conflicts nor change a targeted country’s policies. Indeed, many sanctions regimes have failed to achieve their stated aims even decades after they were imposed. One parallel for the new Russia sanctions can be seen in the even more stringent measures imposed against its ally, Iran.

Iran sanctions, a history lesson

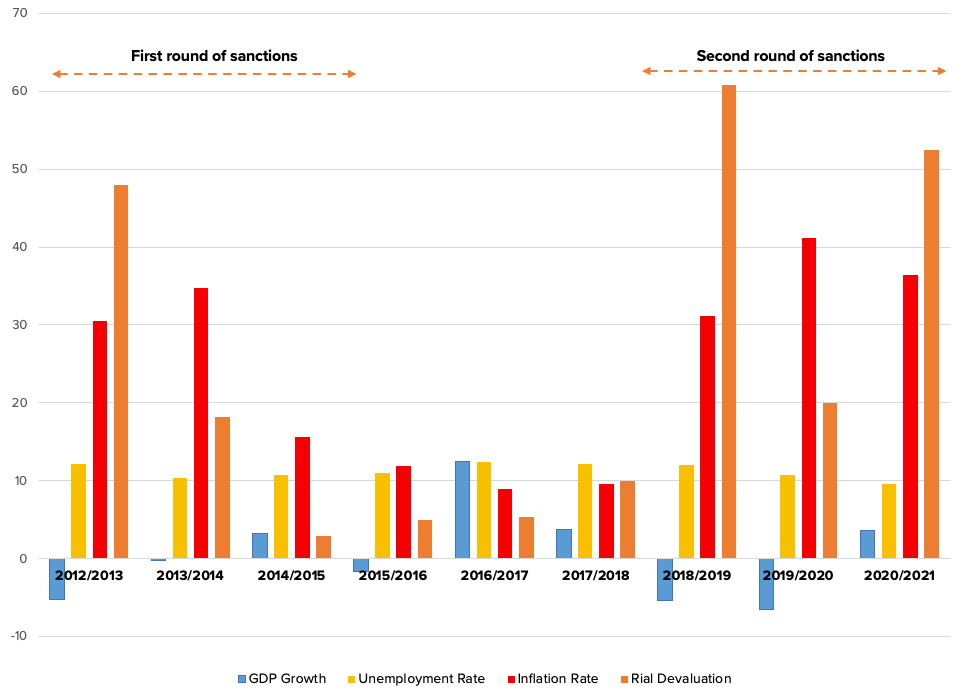

Iran has been under various US sanctions for four decades and experienced severe economic sanctions in two rounds—under the Barack Obama and Donald Trump administrations—largely because of its advancing nuclear program. The first set of restrictive measures were imposed in December 2011, when the US, under the Obama administration, sanctioned Iran’s central bank and required substantial reductions in Iranian oil exports. This was followed in January 2012 by the European Union (EU) announcing that it would scale back and then suspend imports of Iranian oil. The results were dramatic. Iran’s GDP dropped by more than 5 percent in 2012-2013, the Iranian currency rial was devalued by 48 percent, and inflation rose to more than 30 percent from 21.5 percent over a year.

The desire for sanctions relief was a factor in Iran’s willingness to negotiate an interim agreement in 2013 and then a longer-term deal known as the Joint Comprehensive Plan of Action (JCPOA) in 2015, which curbed Iran’s nuclear program in exchange for sanctions relief. However, in 2018, President Trump withdrew from the JCPOA despite Iranian compliance. The US then unilaterally re-imposed all previous sanctions on Iran and even added new ones as part of its “maximum pressure” strategy.

As the multilateral Obama era sanctions continued from 2012 to 2015 (until the signing of the JCPOA), Iran’s GDP decreased by 0.8 percent each year on average, while unemployment and inflation rates were 11.1 percent and 27 percent, respectively. Moreover, the rial devalued significantly by 23 percent each year throughout this time. The oil and natural gas, automotive, shipping, shipbuilding, and aviation industries were the hardest hit. However, once the JCPOA was negotiated and implemented, Iran’s economy rebounded.

Even though the Trump era sanctions were unilateral, they had an initial dramatic impact because of the US-imposed oil embargo and COVID-19 pandemic, which entailed more economic costs. During the pandemic, the drop in oil price created another negative shock to the Iranian economy. However, over time, Iran increased oil exports to 1.7 million barrels per day from the 606,000 barrels per day in February 2020 (selling primarily to China), as the Biden administration looked to rejoin the JCPOA and the oil price recovered. Iran’s economy, as a result, has experienced moderate growth. Interestingly, the International Monetary Fund forecasts Iran’s GDP will grow by 3 percent in 2022.

In the period from the signing of the JCPOA until the US withdrawal (2015 to 2018), Iran’s GDP grew by 4.8 percent and inflation fell to 10.1 percent each year on average, but unemployment stayed high at 11.8 percent, per my calculations. In the second round of sanctions imposed by the Trump administration from 2018 to 2021, GDP decreased again by 2.7 percent each year, unemployment was 10.7 percent, and inflation increased dramatically to 36.2 percent. Furthermore, the rial experienced a large devaluation of 44.4 percent each year on average.

The effects of sanctions on the Iranian economy imply that, depending on the severity and kind of restrictions, sanctions could significantly lower GDP growth and increase foreign exchange rates and inflation in targeted countries. However, unemployment rates remained unaffected by the sanctions because most Iranian employment is in service industries, which aren’t subject to sanctions in the same way petroleum exports are. As a result, economic and financial penalties will be more effective in industries more dependent on international trade and finance.

A comparison of sanctions

With the case of Iran, the multilateral sanctions in the first round were gradually implemented. For example, two months after the US sanctioned the Iranian financial sector, the Society for Worldwide Interbank Financial Telecommunication (SWIFT) stopped sending financial services to Iran’s central bank and other designated Iranian financial institutions. However, with the case of Russia, the punishment was more immediate. US sanctions on Russia’s central bank and a block on several Russian banks from using SWIFT happened within days after the invasion of Ukraine. This dramatically impacted the Russian currency, the ruble, which lost 30 percent of its value in just a few hours. The ruble has since rebounded somewhat, but Russia’s ability to continue to prop up the currency is unclear.

A bigger difference between Russia and Iran is that Moscow was integrated into the global economy. Even after the JCPOA was implemented, few major multinational companies entered the Iranian market for fear of jeopardizing their much more lucrative markets in the US. For Russia, on the other hand, detachment from the global market has been dramatic. Large multinational companies exited the Russian market deliberately to protect their reputations from association with Putin’s abuses; over four hundred multinational companies, including Apple, Facebook, Shell, and BP, have left since the war began.

Furthermore, unlike with Iran, European policymakers are reluctant to impose sanctions on Russia’s energy exports, despite the fact that the Russian economy is similarly reliant on such revenues. Fuel and energy exports accounted for 63 percent of total Russian shipments, with crude oil and natural gas accounting for 26 percent and 12 percent, respectively. Additionally, oil and gas provided 39 percent of Russia’s federal budget revenue in 2019, and Russia is the second-largest crude oil exporter after Saudi Arabia. However, the EU gets 41 percent of its natural gas imports from Russia. Therefore, US and EU policymakers have been very cautious in imposing sanctions on Russian energy exports, which could greatly impact Europe. The fact that Russia is still getting paid for its oil and gas exports—and higher energy prices since Russia’s invasion—might alleviate the impact of current sanctions on the Russian economy.

According to the White House, the Russian economy will contract by as much as 15 percent in 2022 and the inflation rate may rise to 15 percent on a year-over-year basis. The costs are certain to be severe. But, as with the sanctions against Iran, economic pain may not lead to desired policy changes and there is no sign yet that Putin will end his invasion of Ukraine.

Iran, meanwhile, dramatically advanced its nuclear program in response to US sanctions and has yet to agree to return to compliance with the JCPOA. Although it’s too soon to tell with Russia, it’s safe to say that there are clear limits to what economic sanctions can achieve, especially against autocratic regimes whose elites tend to fare much better than ordinary citizens.